Forms 1099-R and 5498: Small Changes, Big Implications for 2026 Reporting

By Jodie Norquist, CIP, CHSP

In late June 2026, the IRS released the final 2026 tax year versions of Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.; Form 5498, IRA Contribution Information, and Instructions for Forms 1099-R and 5498.

At first glance, the updates to Forms 1099-R and 5498 may feel like a form redesign and technical clean-up. But these form updates seem to signal something bigger: a push toward more structured reporting, new distribution types, and a broader modernization trend, making it easier for machines to read, validate, and analyze reporting.

Here are some of the changes for 2026 reporting we feel you should know about if you work with IRAs and employer-sponsored retirement plans.

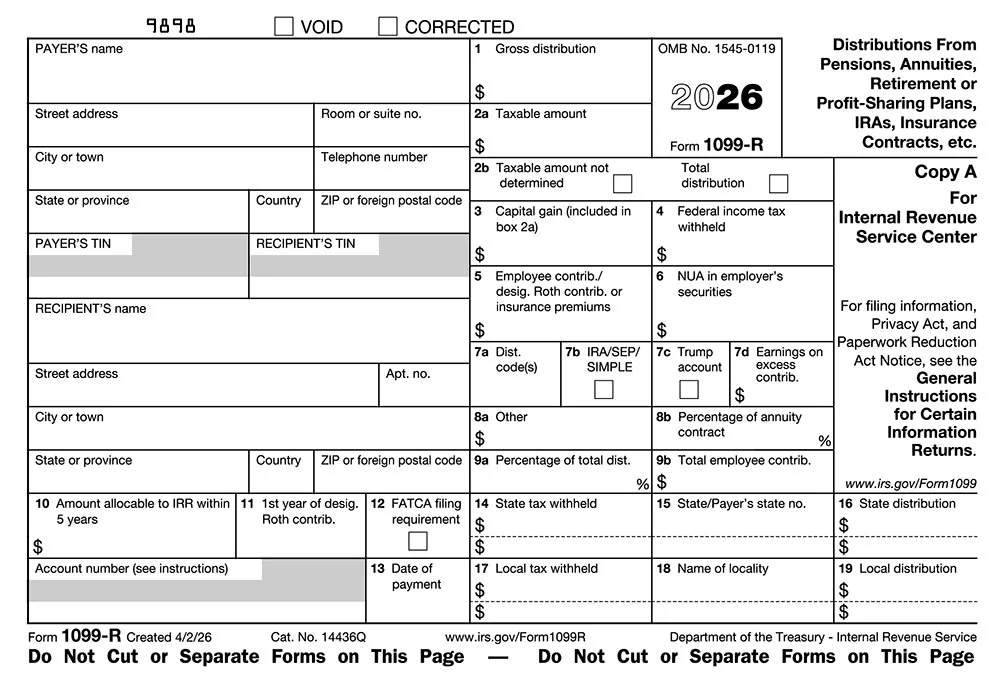

Form 1099-R Notable Changes

Address Fields Have Been Separated

For the payer’s and recipient’s information, the IRS has now separated the address block into individual entry boxes. This standardizes formatting across IRS forms and supports improved electronic processing.

Box 7 Has Expanded Into Separate Sub-Boxes

Your IRA operations teams and retirement plan reporting teams may be most familiar with Box 7 of Form 1099-R, where payer’s post distribution codes. This box has been separated into four sub-boxes.

Box 7a, Dist. Code(s), reports the distribution codes used to identify the type of distribution made.

Box 7b, IRA/SEP/SIMPLE, identifies the type of IRA from which the distribution was taken.

Box 7c, Trump account, identifies distributions from 530A accounts, also known as Trump Accounts.

Box 7d, Earnings on excess contrib., reports earnings attributable to distributed excess contributions made to a 530A account. These earnings are subject to a 100 percent tax.

NOTE: A new form, Form 5498-TA, Trump Account Contribution Information, reports contribution information on 530A accounts.

Code Y for QCDs is Optional for 2026 Reporting

Code Y, Qualified charitable distributions (QCD) claimed by taxpayer under section 408(d)(8), remains optional for 2026 reporting, as it was for 2025. Code Y was introduced in 2025 and may be used in Box 7a when an IRA owner or beneficiary age 70½ or older takes a QCD. When code Y is used, it must appear first and combined with either codes 7, 4 or K, depending on the circumstances of the distribution.

Box 8 Has Been Split into Two Boxes

Box 8 has been separated into Box 8a, Other, and Box 8b, Percentage of annuity contract. Box 8a reports the current actuarial value of an annuity contract included in a lump-sum distribution. If the distribution was made to more than one person, the applicable percentage is shown in Box 8b.

Reporting the actuarial value of a commercial annuity contract in Box 8a is optional for 2026, according to the IRS.

New Code for Qualified Long-Term Care Distributions

Qualified long-term care distributions from defined contribution plans will be reported on Form 1099-R using code 1, in Box 7a. These distributions are taxable but will not be subject to the 10 percent penalty tax.

Charges or payments for a qualified long-term care insurance contract against the cash value of an annuity contract or the cash surrender value of a life insurance contract is reported on Form 1099-R using code W in Box 7a.

NOTE: Qualified long-term care distributions taken from 401(a), 403(b), and governmental 457(b) plans are exempt from the 10 percent early distribution penalty tax. This penalty exception, however, does not apply to IRA distributions.

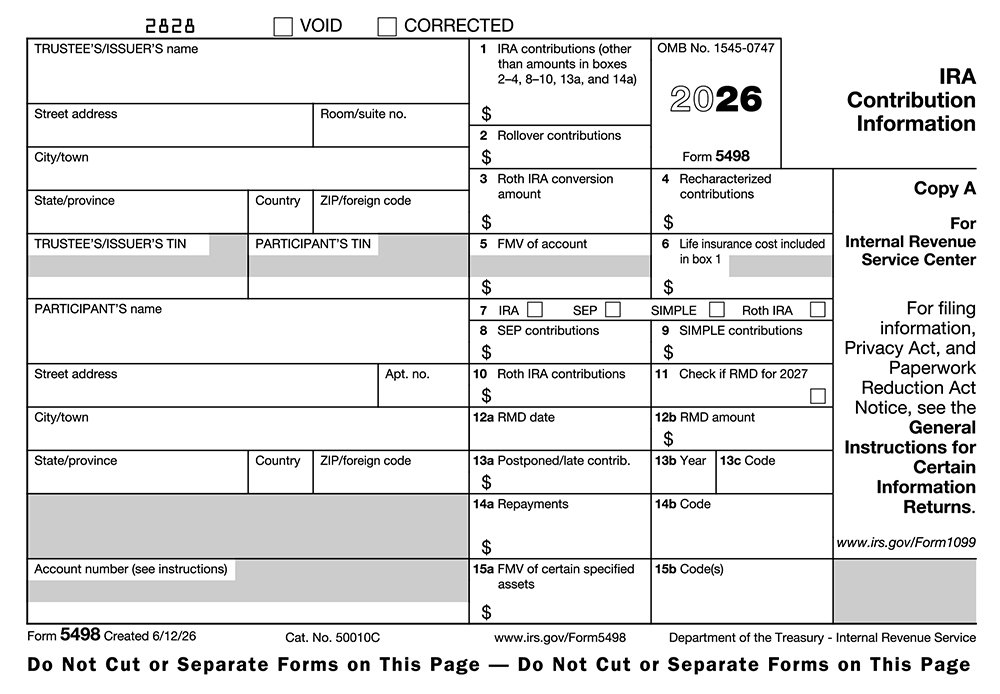

Form 5498 Notable Changes

Address Fields Separated into Individual Entry Boxes

The IRS has added individual data elements (street, city, state, Zip code), rather than a combined block, for trustee’s or issuer’s and participant’s information.

New Code for Repayments of Qualified First-Time Home Purchase Distributions

The IRS has created a new code, HP, to report repayments of qualified first-time home purchase distributions as described in section 72(t)(2)(F). The amount is reported in Box 14a, Repayments, and the code, HP, is reported in Box 14b, Code.

New IRS Publication Available for 2026

Starting for 2026 reporting, the IRS has issued a new publication, Publication 1099, General Instructions for Certain Information Returns. Previously, the publication was named General Instructions for Certain Information Returns. The publication is used to prepare 2026 Forms 1096, 1097, 1099, 3921, 3922, 5498, and W-2G.

Be Prepared for Other 2026 Tax Year Reporting Changes Ahead

For financial organizations, these changes are likely to require system updates to accommodate 2026 reporting requirements.

However, one of the most important changes for 2026 IRA reporting won’t be found on Forms 1099-R and 5498 at all.

Starting with 2026 tax reporting, filed in 2027, the IRS is retiring its FIRE system, replacing it with the IRIS platform for electronic filing. This is a workflow change, not just a compliance update.

Financial organizations will need to register for new credentials, update their file submission processes, and test transmissions well before deadlines. For many organizations, this may be the most disruptive change in the reporting cycle.