What You Need to Know About New Distribution Code Y For Qualified Charitable Distributions

NOTE: On October, 16, 2025, the IRS posted that using code Y in Box 7 is optional for the 2025 Form 1099-R. Financial organizations may choose to, but are not required to, use the new code Y to report qualified charitable distributions for 2025.

By Kristiana Rodriguez, CIP

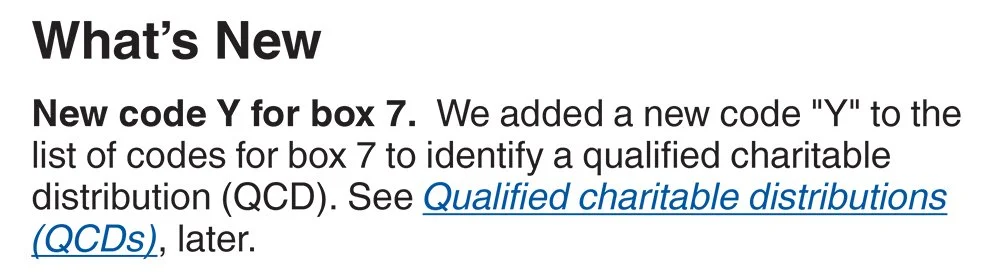

In April, the IRS released the 2025 Instructions for Forms 1099-R and 5498 and surprised us all by announcing a specific code for qualified charitable distributions (QCDs). Historically, these distributions were processed and reported as a normal distribution, code 7, or a death distribution, code 4, on Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc. The following is an excerpt from the 2025 instructions.

The introduction of code Y has brought up a lot of questions. Here’s what we know so far, and what information we hope to see by the end of the year.

Are financial organizations required to report code Y in 2025?

Yes, because the 2025 Form 1099-R instructions reference code Y, we expect that the IRS will require its use. The IRS has given no indication of delaying the use of code Y to a later year.

The IRS has a tiered penalty structure for Form 1099-R reporting failures, which can be applied if the financial organization fails to include the information required to be shown on Form 1099-R, or includes incorrect information on Form 1099-R. For 2025, the penalty is $60 per return if corrected within 30 days, the maximum penalty is $683,000 per year, reduced to $239,000 for small businesses. The penalty increases if corrected after 30 days. For more information on potential penalties, see the General Instructions for Certain Information Returns.

Are other codes used with code Y?

Yes, the Form 1099-R instructions state that code Y must be used with one of the following codes.

• Code 7, Normal distribution, for a QCD taken from a Traditional IRA

• Code 4, Death, for a QCD taken from an inherited Traditional IRA

• Code K, Distribution of traditional IRA assets not having a readily available FMV, for a QCD taken with IRA or inherited IRA assets that do not have a readily available fair market value.

According to the instructions, Code Y will be used first, and the applicable secondary code will follow.

Can we use code Y if we make the check out to a charity but mail the check to the client?

Yes. A client can still personally deliver the check to the charity. The check must be made payable to the charity requested, and not the client.

What if we’ve already processed QCDs in 2025 without using code Y?

You should flag previous QCD transactions processed between January 1, 2025, and whenever your system can properly report code Y with its applicable code. These flagged accounts may have to be manually processed.

How do we set code Y up in our system?

You will need to speak to your core processor to get the new distribution code set up in your system. As previously mentioned, code Y must be used with code, 4, 7, or K, so two codes will need to be generated for your clients’ Forms 1099-R.

Do taxpayers still exclude a QCD from their income reported on IRS Form 1040 when they file their taxes?

The 2025 Form 1040, U.S. Individual Income Tax Return, has not yet been released. Upon its release, we expect to know what, if any, instructions are provided to taxpayers regarding QCDs. It has previously been up to taxpayers to exclude any QCDs from their taxable income and include a code (“QCD”) on their Form 1040 explaining that exclusion.

How do you report a Roth QCD?

Because qualified Roth IRA distributions are distributed tax free, a QCD taken from a Roth IRA will have no beneficial tax effect unless earnings are being distributed in a nonqualified distribution. Code Q, Qualified distribution from a Roth IRA, code T, Roth IRA distribution, exception applies, and code J, Early distribution from a Roth IRA, no known exception, are used to report Roth IRA distributions. The IRS has not yet provided guidance on how to report QCDs taken from Roth IRAs.

Is there still an age requirement for a QCD?

Yes, IRA owners and beneficiaries must be age 70½ or older to make a QCD. Although the applicable RMD age is currently 73, the minimum age requirement for QCD remains unchanged.

What is the 2025 limit for QCDs?

It is $108,000 (indexed for cost-of-living adjustments). For married couples, the limit applies separately to each spouse.

The Secure 2.0 Act allows QCD-eligible individuals to make a one-time tax-free donation of up to $54,000 (indexed) to a “split interest entity” (charitable gift annuities, charitable remainder unitrusts, and charitable remainder annuity trusts). This $54,000 limit appears to be within the overall $108,000 annual limit (as indexed) for 2025 and is subject to certain restrictions. The remainder of the annual limit could be contributed as a QCD to a qualified charitable organization in the normal manner.

Should we use a specific form for QCDs?

Although the IRS does not require financial organizations to use a certain form, Ascensus does offer Form #22, Charitable Distribution Request, that your organization can use to document QCDs. Ascensus is also in the process of updating its withdrawal form to include QCDs as a withdrawal reason. It is a business decision if you use a specific or general form to process QCDs. Whatever your process is, you’ll want to document the procedure and train your team.

We will continue to review any new information that the IRS releases about code Y and any changes made to the financial organization’s responsibilities for processing QCDs.