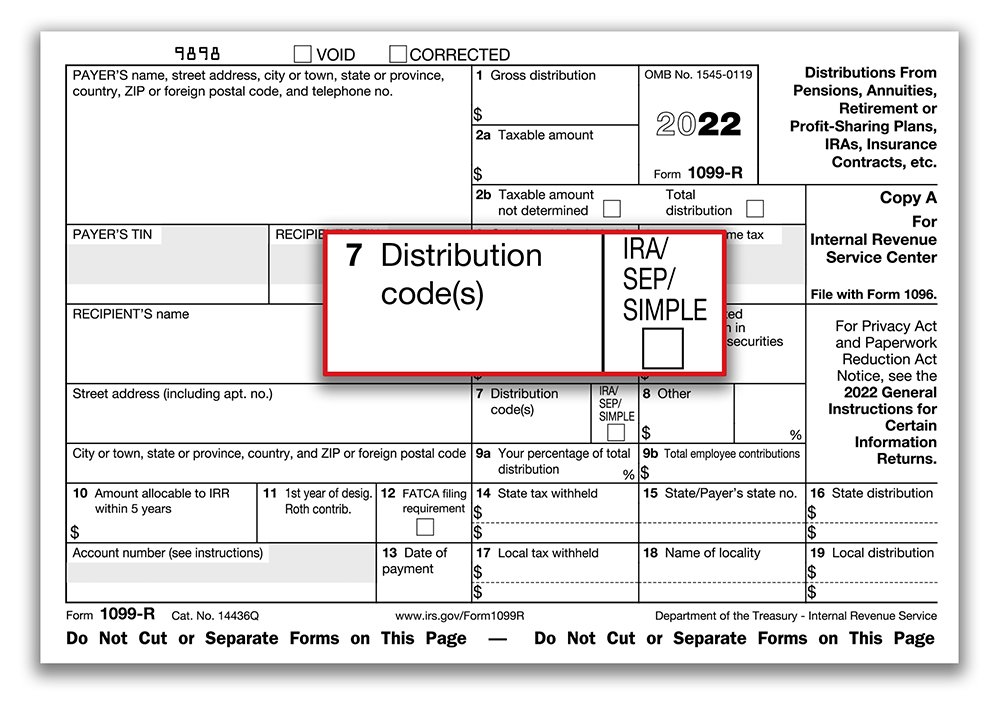

Selecting the Correct IRS Form 1099-R Box 7 Distribution Codes

A common compliance mistake occurs when financial organizations use the incorrect distribution code in Box 7, Distribution code(s), on IRS Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.

IRA owners and qualified retirement plan (QRP) participants who take distributions during a given tax year must receive a Form 1099-R reporting that distribution by January 31 of the following year. Financial organizations and plan administrators must also send these forms to the IRS.

If you’re stumped on which code to use in a specific circumstance, here are the codes and explanations that apply to IRA and QRP distributions.

Code 1

Use Code 1, Early distribution, no known exception, for Traditional and SIMPLE IRAs and QRPs only if the individual is under age 59½ and codes 2, 3, and 4 do not apply. Use even if the individual is withdrawing the money for one of the following penalty tax exceptions: unreimbursed medical expenses that exceed 7.5 percent of adjusted gross income, health insurance following unemployment, qualified higher education expenses, qualified first-time homebuyer expenses, qualified reservist distributions, or qualified birth or adoption distributions.

Use Code 1 if the individual modified a series of substantially equal periodic payments before the end of the five-year period that began with the first payment, even if he is age 59½ or older.

Code 1 may be used with codes 8, B, D, K, L, M, or P.

Code 2

Code 2, Early distribution, exception applies, lets the IRS know that the individual is under age 59½ but that she qualifies for certain exceptions.

Use code 2 for a Traditional or SIMPLE IRA distribution when

the IRA owner directly converted the assets to a Roth IRA;

the distribution was a result of an IRS levy;

the distribution was part of a series of substantially equal periodic payments; or

the individual qualifies for a penalty tax exception that doesn’t require using codes 1, 3, or 4.

Use code 2 for a QRP distribution when

the distribution was the result of an IRS levy;

the plan participant separated from service during or after the year he attained age 55;

the distribution was part of a series of substantially equal periodic payments;

the distribution was a permissible withdrawal under an eligible automatic contribution arrangement;

the plan participant qualifies for a penalty tax exception that does not require using codes 1, 3, or 4;

it is a governmental 457(b) plan distribution that is not subject to the 10 percent early distribution penalty tax; or

it is a distribution from a governmental defined benefit plan to a public safety employee after separation from service, in or after the year the employee reached age 50.

Code 2 may be used with codes 8, B, D, K, L, M, or P.

Code 3

Use code 3, Disability, when proof of disability is provided at the time of distribution. Verification is not required by the IRS, but is highly recommended. If no proof is provided, the financial organization should enter code 1 in Box 7 (the individual can file Form 5329, Additional Taxes on Qualified Plans (Including IRAs) and Other Tax-Favored Accounts, to still use the disability exception).

Individuals claiming disability to avoid the early distribution penalty tax must qualify as disabled within the meaning of Internal Revenue Code Section (IRC Sec.) 72(m)(7). Some disabled individuals file IRS Schedule R, Credit for the Elderly or the Disabled, with their tax return. The Schedule R instructions include a Physician’s Statement that may be used to verify that the individual is permanently and totally disabled. Financial organizations may ask IRA owners for a copy of the signed Physician’s Statement or an equivalent statement signed by a physician before using code 3.

Code 3 may be used with code D.

Code 4

Always use code 4, Death, when distributions are made to a beneficiary (including an estate or trust) after a Traditional or SIMPLE IRA owner’s or plan participant’s death.

Code 4 may be used with code 8, A, B, D, G, H, K, L, M, or P.

Code 5

Only use Code 5, Prohibited transaction, when an IRA prohibited transaction has occurred. This tells the IRS that the account is no longer an IRA. The distribution amount shown should equal the IRA’s fair market value on the first day of the tax year that the prohibited transaction occurred.

Code 5 should not be used with any other codes.

Code 7

Use code 7, Normal distribution, when the IRA owner or plan participant is age 59½ or older (use code 1 if the individual is age 59½ or older but modified a series of substantially equal periodic payments before five years).

Code 7 may be used in combination with codes A, B, D, K, L, or M.

Code 8

According to the 2022 Instructions for Forms 1099-R and 5498, Code 8, Excess contributions plus earnings/excess deferrals (and/or earnings) taxable in 2022, signifies that excess contributions were deposited and returned in the same year (regardless of the year for which the excess was attributed). For example, use code 8 to report a contribution deposited in April 2022 for tax year 2021 and later removed in 2022.

Code 8 may be used with codes 1, 2, 4, B, J, or K.

Code 9

Use Code 9, Cost of current life insurance protection, to report premiums paid by a QRP trustee or custodian for current life or other insurance protection.

Code 9 should not be used with any other codes.

Code A

Use Code A, May be eligible for 10-year tax option, to indicate that a lump-sum distribution received by a plan participant born before January 2, 1936 (or their beneficiaries), may be eligible for 10-year income averaging tax treatment.

Code A may be used with code 4 or 7.

Code B

Enter code B, Designated Roth account distribution, to report distributions from a designated Roth account, unless the distribution is a direct rollover to a Roth IRA or is because of a correction under the Employee Plans Compliance Resolution System.

Code B may be used with codes 1, 2, 4, 7, 8, G, L, M, P, or U.

Code E

Use code E, Distributions under Employee Plans Compliance Resolution System (EPCRS), if excess employer contributions and applicable earnings under a SEP or SIMPLE IRA plan are returned to the employer (with the IRA owner’s consent).

Code E should not be used with any other codes.

Code G

Enter code G, Direct rollover and direct payment, when plan participants or IRA owners directly roll over non-Roth QRP or IRA assets to an eligible employer-sponsored retirement plan. Also use when non-Roth QRP assets are directly rolled over to an IRA, and for in-plan Roth rollovers that are direct rollovers.

Code G may be used with codes 4, B, or K.

Code H

When reporting designated Roth account distributions that are directly rolled over to a Roth IRA, enter code H, Direct rollover of a designated Roth account distribution to a Roth IRA.

Code H may be used in combination with code 4.

Code J

Use Code J, Early distribution from a Roth IRA, to report a Roth IRA distribution when the IRA owner is under age 59½ and codes Q and T do not apply. But use code 2 for an IRS levy and code 5 for a prohibited transaction. Code J should be used if the Roth IRA owner meets the five-year waiting period but the distribution is not qualified because the IRA owner is not yet age 59½, has not died, or is not disabled. Use code J to report a qualified distribution for first-time homebuyer expenses. Also use code J if a Roth IRA owner modified a series of substantially equal periodic payments before being eligible to do so.

Code J may be used with code 8 or P.

Code K

Use code K, Distribution of traditional IRA assets not having a readily available FMV, to report IRA distributions of assets that do not have readily available fair market values, such as for the following.

Stock, other ownership interest in a corporation, short or long-term debt obligations, not readily tradable on an established securities market

Ownership interest in a limited liability company, partnership, trust, or similar entity (unless the interest is traded on an established securities market)

Real estate

Option contracts or similar products not offered for trade on an established option exchange

Other asset that does not have a readily available FMV

Code K may be used with codes 1, 2, 4, 7, 8, or G.

Code L

Do not use code L, Loans treated as deemed distributions under section 72(p), to report a plan loan offset. See “Loans Treated as Distributions” in the 2022 Instructions for Forms 1099-R and 5498.

Code L may be used with codes 1, 2, 4, 7, or B.

Code N

Code N, Recharacterized IRA contribution made for 2022, should be used when a Traditional or Roth IRA contribution made for 2022 was recharacterized in 2022 (a “same-year” recharacterization).

Code N should not be used with any other codes.

Code P

Code P, Excess contributions plus earnings/excess deferrals (and/or earnings) taxable in 2021, signifies that excess contributions were deposited in 2021 and returned in 2022. For example, use code P to report a contribution deposited in October 2021 and later removed with NIA in 2022 before the IRA owner’s tax return due date, plus extensions.

Code P may be used with codes 1, 2, 4, B, or J.

Code Q

Only use Code Q, Qualified distribution from a Roth IRA, when the IRA owner has met the five-year waiting period and is either age 59½ or older, has died, or is disabled (assuming there is proof of the disability).

Although first-time homebuyer expenses are considered one of the four distribution reasons that make a Roth IRA distribution qualified when the five-year waiting period has been met, it typically would not be known by the distributing organization whether the first-time homebuyer exception applies. Thus, code J should be used. (Individuals account for qualified distributions made for first-time homebuyer purposes on Form 8606, Nondeductible IRAs.)

Code Q should not be used with any other codes.

Code R

Use code R, Recharacterized IRA contribution made for 2021, when a Traditional or Roth IRA contribution made for 2021 was recharacterized in 2022 (a prior-year recharacterization).

Code R should not be used with any other codes.

Code S

Use code S, Early distribution from a SIMPLE IRA in the first 2 years, no known exception, to report a SIMPLE IRA distribution made within the first two years of participation if the SIMPLE IRA owner is under age 59½ and none of the early distribution penalty tax exceptions apply. If the SIMPLE IRA owner is age 59½ or older, use code 7. If another penalty tax exception does apply, generally use code 2. But use code 3 if the disability exception applies or code 4 if the distribution is paid to a beneficiary. If the SIMPLE IRA owner is under age 59½ and it is after the two-year period, the organization should use code 1. The two-year period begins on the day that the first contribution under the employer’s SIMPLE IRA plan was made to the SIMPLE IRA.

Code S should not be used with any other codes.

Code T

Use code T, Roth IRA distribution, exception applies, to report Roth IRA distributions before the five-year waiting period has been satisfied (or if it’s not known whether the period has been satisfied), but the IRA owner is at least age 59½, has died, or is disabled (assuming there is proof of the disability).

Code T should not be used with any other codes. If any other codes apply, such as code 8 or P, then code J should be used.