New RMD Rule Could Affect Spouse Beneficiaries, Hypothetically

By Mike Rahn, CISP

The surviving spouse of an IRA owner or retirement plan participant has historically had more generous options and greater flexibility than other beneficiaries who might inherit a tax-qualified retirement account. This is understandable, given the fact that retirement security is typically a matter of mutual consequence for married couples.

This mutuality has also been reflected in the requirement that spouses receive protection and priority when beneficiaries are named. It is reflected more broadly in the judicial area, such as the tendency of courts to split retirement accumulations between spouses when divorce occurs, often irrespective of who accumulated the assets before the divorce. Spouses typically get the benefit of the doubt, you might say.

Recently issued IRS final required minimum distribution (RMD) regulations are consistent with this historical bias toward spouses. They generally maintain prior spouse beneficiary distribution options, add a 10-year distribution period option, while also creating new limitations for most nonspouse beneficiaries. These changes reflect provisions of the SECURE Act of 2019.

That said, these new RMD regulations are not without at least one limitation for spouse beneficiaries, in the form of the “hypothetical RMD.” This could affect a spouse beneficiary who inherits an IRA or qualified retirement plan account before the deceased’s RMDs are required to begin—generally age 73—and who elects the new 10-year beneficiary payout rule in order to delay the onset of required distributions.

Spouse beneficiaries might choose this 10-year payout option if they are less than 10 years from RMD age, rather than immediately treating the inherited account as their own, or transferring to their own IRA, as spouses are permitted to do. If spouse beneficiaries immediately treat the account as “their own,” then their RMDs would begin when they reached age 73, a period perhaps significantly less than 10 years. Thus, the choice to use the 10-year option.

Absent the new hypothetical RMD provision, spouse beneficiaries could elect the 10-year option, wait until as late as the ninth year to make the account “their own,” and thereby delay payouts until potentially well beyond the year in which they turned age 73. This tactic was previously allowed under the prior RMD regulations (before the SECURE Act changes), but if an account owner died before starting RMDs, the optional payout period was limited to just five years. Now, if not for the hypothetical RMD provision of these final regulations, the statutory change to 10 years could result in a significant delay in taxation, at least in some cases.

The Hypothetical RMD in Concept

It’s clear that the final RMD regulations permit spouse beneficiaries of IRA owners or retirement plan participants not already in distribution status to use the 10-year rule, to treat the account as their own at any time before the 10th year, and thereby delay RMDs from that account; potentially until well after they have reached the current RMD age of 73.

But now, before spouse beneficiaries can reconfigure an account as “their own,” either by transfer, rollover, or simply renaming the account, the inheriting spouse beneficiary must calculate and distribute from the account “hypothetical RMDs” (a new official term) for all years between when she reached—or when her deceased spouse would have reached the applicable RMD age.

The relative ages of the decedent and the beneficiary are significant only in determining the first year for which a hypothetical RMD is calculated. In other words, which spouse is older makes no difference. The first calculation year is the LATER of the year that the original account owner would have reached RMD age, or the year the beneficiary reached—or will reach—RMD age.

Actual end-of-year account balances for each separate calculation year are not required. Instead, the regulations specify that the balance on December 31 before the year in which the beneficiary makes the account his own will be the starting point. This balance will be reduced for each subsequent calculation after the first, as well as for other distributions—if they have occurred—taken in that year by the beneficiary.

EXAMPLE 1:

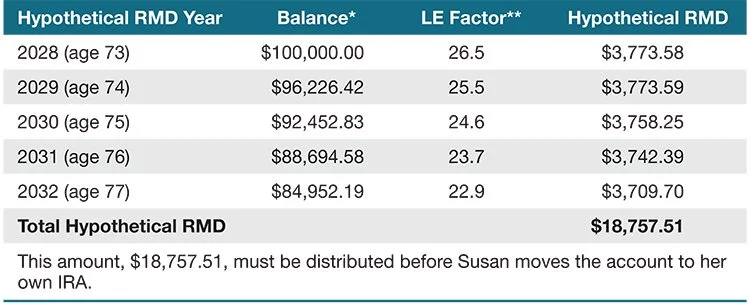

Susan Jones, age 68, inherits a Traditional IRA from her husband Tom, who died in 2023 at age 71. She wishes to delay her RMDs, and understands that electing the 10-year beneficiary payout option will allow her to avoid taking required distributions for nine years—until age 77. She can then treat the account as her own and begin taking RMDs.

However, the new RMD provision of the final regulations will require that before the account becomes “her own” in year nine, which is 2032, hypothetical RMDs will have to be calculated and distributed for several intervening years—including 2032—using the Uniform Lifetime Table.

Year one of the calculation will be the later of the year that Susan would have reached the RMD age of 73 (2028), or the year her husband would have reached age 73 (2025). Clearly in this example, it will be based on Susan’s RMD age.

Accordingly, Susan must calculate and distribute hypothetical RMDs for five years (2028 through 2032) before moving the account to her own IRA. The December 31, 2031, balance, which is $100,000, is the only actual December 31 balance used in the calculations because it occurs immediately before the year that Susan treats the account as her own. This balance is used to calculate the first year’s hypothetical RMD. For subsequent years’ calculations, that balance is reduced for each year’s hypothetical RMD, and takes into account distributions that she might have already taken during any of such years.

Calculation for Example 1: In year of death, deceased IRA owner is age 71, spouse beneficiary is age 68

NOTE: As in any RMD calculation, the prior-year’s December 31 balance—in these calculations a hypothetical balance— is divided by the life expectancy factor to determine the hypothetical RMD for the year.

This hypothetical RMD amount, $18,757.51, must be distributed before Susan moves the account to her own IRA.

*The beginning balance is the December 31 balance occurring immediately before the year in which the beneficiary makes the account her own. Because Susan made the account her own in 2032, the December 31, 2031, balance must be used for the beginning balance.

**Based on the Uniform Lifetime Table

EXAMPLE 2:

Now for comparison purposes, imagine that Susan and Tom’s ages are reversed. Susan is age 71 when she inherits Tom’s Traditional IRA after he dies in 2023 at age 68. She wishes to delay RMDs under the 10-year rule, and take no distributions until year nine (2032), when she will be 80, after which she will treat the account as her own.

Hypothetical RMDs must be calculated and distributed before she can treat the account as her own. The first calculation year—as was the case in Example 1—will be the later of the year she would have reached age 73 (2025) or the year her deceased spouse would have been age 73 (2028).

Just as in Example 1, hypothetical RMDs must be calculated for the same five years (2028 through 2032), illustrating the fact that it does not matter which of the two individuals is older, since the first year of the calculations will be the “later of” the years in which the respective spouses reach—or would have reached—RMD age.

The key difference in Example 2 is that the age and life expectancies for these five years will be those of the beneficiary, who is older than the deceased IRA owner. If using the same initial balance of $100,000, this will yield larger hypothetical RMDs for all years.

Calculation for Example #2: In year of death, deceased IRA owner is age 68, spouse beneficiary is age 71

This hypothetical RMD amount, $20,832.63, must be distributed before Susan moves the account to her own IRA.

NOTE: The final regulations provide that the hypothetical RMD rule does not apply to a surviving spouse beneficiary who is subject to the five-year rule. However, the five-year rule would not apply to a spouse beneficiary for any death year after 2019, which makes the point moot now.