Successful IRA Programs Depend on Knowing How Traditional and Roth IRAs Differ

by Jennifer Bassett, CIP, CISP, QKA

In today’s competitive market, financial organizations that are a trusted go-to source for IRA information will attract more clients and build account balances. And IRA balances are still growing strong. It is estimated that by the end of 2017, Traditional IRA assets were worth approximately $7.85 trillion, Roth IRA assets were worth $810 billion, and the grand total of all IRA assets was $9.2 trillion, up from the year before, according to the Investment Company Institute’s Report: The U.S. Retirement Market, Second Quarter 2018.

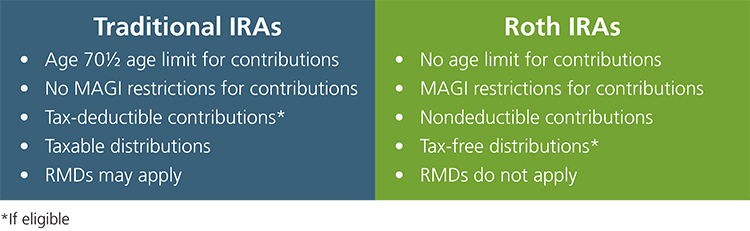

Successful IRA programs depend on staff being able to talk intelligently—without giving tax advice—about IRAs, particularly about the differences between Traditional and Roth IRAs. The differences fall into two main categories: contributions and distributions.

Contributions

Eligibility

The contribution eligibility requirements generally differ between Traditional and Roth IRAs. But one requirement applies to both: having earned income. To make a Traditional or Roth IRA contribution, the IRA owner (or spouse, if married and filing a joint income tax return) must be actively working and receiving compensation for the year that the contribution is made for.

Roth IRA

In addition to earning compensation, to be eligible to contribute to a Roth IRA, an individual’s or married couple’s modified adjusted gross income (MAGI) must be below certain limits ($135,000 for a single filer and $199,000 for a married joint filer for 2018).

Traditional IRA

While the law does not limit Traditional IRA contribution eligibility based on income, it does impose a maximum age restriction. Traditional IRA owners are not allowed to make contributions once they attain age 70½. For instance, an IRA owner who turns 70½ on November 10, 2018, cannot make a Traditional IRA contribution for 2018, or for any subsequent year.

Tax-Deductible Contributions

The ability to make tax-deductible contributions is one of the Traditional IRA’s main selling points. (Roth IRA contributions are never tax-deductible.) Whether a Traditional IRA contribution is deductible depends on the IRA owner’s active participation in an employer‐sponsored retirement plan, marital status, and MAGI.

Even if Traditional IRA contributions are not tax‐deductible, eligible individuals still may contribute up to the applicable annual limit. Nondeductible Traditional IRA contributions create after‐tax assets in the IRA that are not taxed when distributed. For individuals that exceed the Roth IRA income limits, a nondeductible Traditional IRA contribution may be the only IRA contribution they can make.

Distributions

Once contributed, Traditional and Roth IRA assets both grow tax-deferred. How IRA assets are later distributed and taxed varies greatly between Traditional and Roth IRAs.

Roth IRA Distributions

Roth IRA assets must be distributed in the following order: regular contributions, conversion and retirement plan rollover assets, and earnings.

Qualified Roth IRA distributions are tax- and penalty-free. This is probably the biggest advantage of a Roth IRA. For distributions to be qualified, a five-year period must be met and the Roth IRA owner must be age 59½ or older, a first-time homebuyer, disabled, or deceased. If not qualified, the distributions may be subject to income tax and the 10 percent early distribution penalty tax.

Traditional IRA Distributions

Traditional IRA assets generally are taxed in the year distributed. If distributed before an IRA owner attains age 59½, the early distribution penalty tax may apply, unless the IRA owner has a penalty tax exception.

Traditional IRA owners must begin taking annual required minimum distributions (RMDs) beginning with the year they turn 70½. Roth IRA owners do not have to take RMDs. But similar to Traditional IRA beneficiaries, Roth IRA beneficiaries may be subject to annual life expectancy payments upon the IRA owner’s death.

Side-by-Side

Being aware of the main differences between a Traditional IRA and a Roth IRA makes helping clients determine which type of IRA is best for them less complicated.

Education is Available

IRA programs need knowledgeable staff who can accurately answer IRA questions with confidence. Ascensus’ IRA education offerings can help expand knowledge, achieve an industry certification, and grow IRA business.