RMD Odds and Ends

By Ben Maas, CIS, CIP, CISP

As 2025 draws to a close, here are some RMD scenarios you may encounter at your financial organization.

One of our clients opened a Traditional IRA in the year that she turned 73 by making a prior-year contribution. As such, her new IRA does not have a prior December 31 year-end balance. Is she required to take an RMD if she does not have a prior year-end balance to calculate the RMD amount?

No—not in this case. The RMD rules do not require financial organizations to add any regular contributions made after December 31 (i.e., prior-year contributions) to the year-end balance. When there is no December 31 balance to calculate an RMD, an RMD is not due.

We have another client who satisfied his 2024 RMD before closing out his IRA on December 15, 2024. On January 20, 2025, he rolled over the distribution to a new Traditional IRA. His new IRA does not have a prior December 31 year-end balance. Can he avoid taking his 2025 RMD because there’s no prior year-end balance?

While the RMD rules do not require financial organizations to add prior-year regular contributions to the December 31 balance, the rules do require adding rollovers to the December 31 balance. In this case, the IRA owner must take an RMD, calculated by adding the rollover amount to the prior December 31 year-end balance and dividing that figure by the applicable denominator from the appropriate life expectancy table (usually the Uniform Lifetime Table).

A Traditional IRA owner in RMD status has said that she doesn’t need the money, and would rather not take an RMD. Does she have any options?

Although your client must take an RMD, if she doesn’t need the money she can choose to make a qualified charitable distribution (QCD). IRA owners and beneficiaries age 70½ or older* are allowed to make QCDs of up to $108,000 for 2025 and $111,000 for 2026. As long as the check is made payable to the qualified charity, the distribution will not be taxable to the IRA owner.

*While the RMD age is now 73, the minimum age for QCDs remains unchanged.

Does our financial organization face any special QCD reporting requirements for 2025?

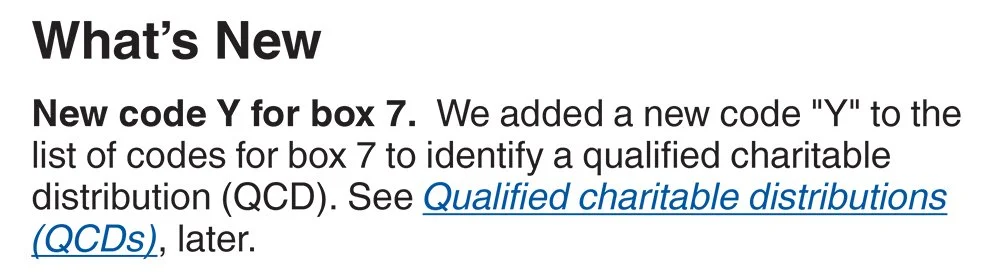

For a time, that appeared to be the case. In April, the IRS released the 2025 Instructions for Forms 1099-R and 5498 and announced a specific QCD reporting code. Historically, these distributions were processed and reported as a code 7, Normal distribution, or code 4, Death, on Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc. The following is an excerpt from the 2025 instructions.

But in October 2025, the IRS released a post clarifying that using code Y is optional for the 2025 Form 1099-R. Financial organizations may choose, but are not required, to use the new code Y to report QCDs for 2025.

Our staff spent a lot of time going back and tracking QCDs that took place between January and April. And we worked tirelessly with our data processor to make sure that we could report QCDs using distribution code Y. Can we still use code Y to report QCDs taken in 2025?

Yes—that is perfectly fine. You must also use one of the following codes with code Y.

Code 7, Normal distribution, to report a QCD taken from a Traditional IRA

Code 4, Death, to report a QCD taken from an inherited Traditional IRA

Code K, Distribution of traditional IRA assets not having a readily available FMV, to report a QCD taken with IRA or inherited IRA assets that do not have a readily available fair market value.

According to the instructions, Code Y will be used first, and the applicable secondary code will follow.