SECURE Legislation Enhances Tax Benefits for Small Employers

By Mike Rahn, CISP

For many businesses, employee perks like retirement benefits may be desirable, but are secondary to maintaining everyday operations and ensuring profitability. This is especially true for small employers.

Lawmakers in Congress have gradually but steadily established and enhanced beneficial tax credits to help and incentivize small employers provide retirement plan benefits for their employees. The first of these was the retirement plan start-up tax credit, enacted in the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA), later made permanent by the Pension Protection Act of 2006 (PPA).

This EGTRRA/PPA provision offered a tax credit of up to 50 percent of qualified start-up costs—to a maximum of $500 per year—for up to three years. It was offered to “small” employers, defined as those having no more than 100 employees that received $5,000 or more from the employer for the preceding year. To claim the start-up credit, the employer must have at least one “non-highly compensated” employee.

NOTE: For 2026, a non-highly compensated employee is someone who either 1) was not a five percent owner* at any time during the 2026 plan year or the 2025 plan year, or 2) did not earn more than $160,000 in 2025. (To be considered a five percent owner, an individual must actually own (or be considered to own) more than five percent of the employing entity.)

Qualified start-up costs are defined as ordinary or necessary expenses that are paid, or incurred, in connection with the plan’s establishment, administration, or retirement-related education for employees. Costs incurred in one year that exceed the allowable credit cannot be carried over to a subsequent year.

The retirement plans that qualify for this small employer tax credit include 401(a) defined contribution plans (including 401(k) plans), defined benefit (DB) plans, 403(a) annuity plans, and SEP and SIMPLE IRA plans.

NOTE: A tax credit is preferable to a tax deduction of the same amount, because a credit reduces a tax obligation dollar-for-dollar, whereas a deduction only reduces taxable income.

Larger Start-Up Credit, Auto-Enrollment, and Contribution Credits

The SECURE Act of 2019—often referred to as SECURE 1.0—and subsequent legislation known as SECURE 2.0, enacted in 2022, have enhanced the start-up credit and added credits for automatic enrollment and for employer contributions to these plans.

Automatic Enrollment Credit

SECURE 1.0 created an automatic enrollment credit for new or existing small 401(k) or SIMPLE IRA plans that include, or add, an automatic enrollment feature. Under automatic enrollment, newly-eligible employees automatically have amounts withheld from their pay at a plan-defined rate, unless they affirmatively opt out or choose a different deferral rate. The automatic enrollment credit is $500 per year, for three years.

SECURE 1.0 Enhancements to Start-Up Credit

SECURE 1.0 raised the maximum small plan start-up credit ten-fold, from $500 to $5,000, while retaining the same limitation of 50 percent of qualified start-up expenses, the same qualified expense definition, and the same retirement plans to which the credit applies.

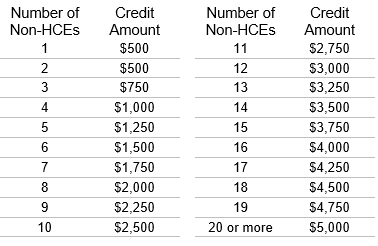

SECURE 1.0 also added a new element to the tax credit calculation process, a graduated scale of maximum credit amounts based on the number of non-HCEs in an employee population. The net effect is to give a greater credit to an employer whose employee population has more non-HCEs, compared to employers who—with the same number of employees—have fewer non-HCEs.

SECURE 2.0 Adds More Start-Up Credit Enhancements

Under SECURE 2.0, smaller eligible plans—those with no more than 50 employees—are now potentially eligible for a 100 percent tax credit for start-up expenses. Employers with 51 to 100 employees remain limited to a maximum tax credit of up to 50 percent of eligible start-up expenses. For all employers, the basic calculation is compared to the non-HCE graduated scale, and the lesser amount is the employer’s tax credit (see below).

New Employer Contribution Credit

In addition to modifying the new plan start-up tax credit structure, SECURE 2.0 provides a new tax credit for employer contributions made on behalf of employees in newly established plans. It applies to all of the retirement plan types that are eligible for the start-up credit, except defined benefit (DB) pension plans. The credit can be claimed for five years, rather than three, but is tiered, with gradually decreasing credits after year two.

Like the plan start-up credit, a distinction is made between smaller and larger employers. The employer contribution tax credit uses the same employer-size break-point—1 to 50, and 51 to 100—and is gradually phased-out for employers with 51 to 100 employees. For both small and large employers, no credit is available for employees with more than $100,000 in FICA wages.

Conditions include the following.

Employers with 1 to 50 employees

Credit claimed cannot exceed 100 percent of the employer contribution

Credit is limited to $1,000 per eligible employee in years one and two

Credit per eligible employee is reduced to 75 percent in year three, 50 percent in year four, 25 percent in year five

Employers with 51 to 100 employees

As noted above, the contribution credit is gradually phased out for employers with 51 to 100 employees. The maximum credit as calculated under the five-year schedule is further reduced by two percent for each employee above the 50-employee threshold, for all years.

Example: Assume that XYZ Company has 70 employees, and they all make under $100,000 in FICA compensation. XYZ Company makes a $1,500 contribution to each employee.

To determine the contribution credit in the first year of the employer’s eligibility, XYZ Company multiplies 70 employees by the $1,500 contribution for a total of $105,000, which multiplied by the applicable percentage of 100% is still $105,000. However, because the employer cannot receive a credit for more than $1,000 per employee, the credit is reduced to $70,000. Further, because XYZ Company has over 50 employees, it must reduce the amount of the credit by multiplying the number of employees over the 50-employee limit (20) by 2% for a total of 40%. XYZ Company must then multiply $70,000 by 40% to determine the amount by which the credit must be reduced, which is $28,000. The credit for the first year equals $42,000 ($70,000 - $28,000).

Key Takeaway

Many American workers still lack a workplace retirement plan. Congress and policy makers continue to look for ways to close the so-called “retirement savings gap.” Employer tax credits have for the last quarter century been one of the most consistently employed tools being used by policy makers to address this shortfall.