IRA Beneficiary Options for Deaths On or After January 1, 2020

Updated on February 18, 2026

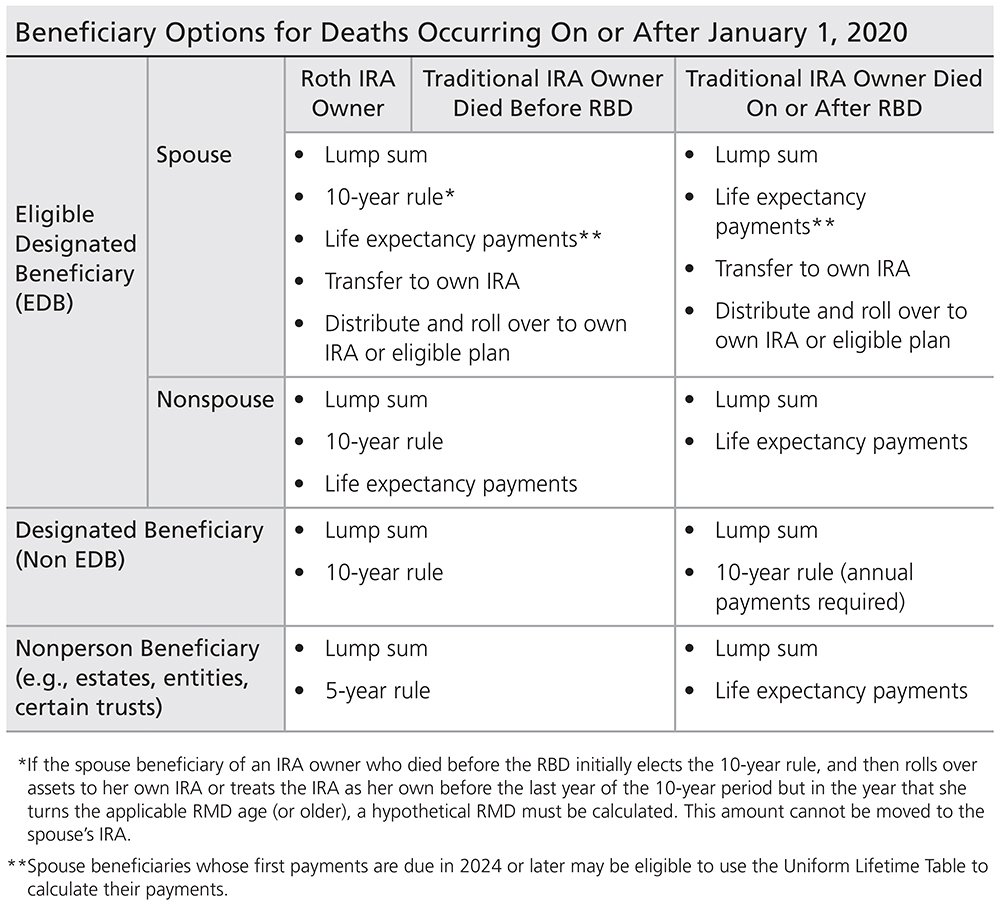

The distribution options available to IRA beneficiaries depend first on whether the IRA owner died before, or on or after January 1, 2020.

If on or after January 1, 2020, the distribution options then depend on whether the beneficiary is an “eligible designated beneficiary,” a “designated beneficiary,” or a “nonperson beneficiary.”

An “eligible designated beneficiary” is the IRA owner’s spouse, the IRA owner’s minor child, a disabled individual, a chronically ill individual, or an individual who is not more than 10 years younger than the IRA owner. The final RMD regulations expand the EDB definition to include beneficiaries of account owners who died before January 1, 2020. EDB determination is made at the time of the IRA owner’s death.

The deceased IRA owner’s minor child must disburse under the 10-year rule once she reaches the age of majority. The “age of majority” has been defined as age 21 under the final RMD regulations. Additionally, the final regulations clarified that a child will include stepchildren, adopted children, and foster children as defined in IRC. 152(f)(1).

A “designated beneficiary” is an individual that is not an eligible designated beneficiary.

A “nonperson beneficiary” is a beneficiary that is not an individual (e.g., an estate or a charity).

Whether the IRA owner died before, or on or after his required minimum distribution (RMD) beginning date (RBD)—or if the IRA is a Roth IRA—only makes a difference if the beneficiary is a nonperson beneficiary, as shown below.

NOTE: There are special rules for certain applicable multi-beneficiary trusts for disabled or chronically ill beneficiaries and for certain annuities.